The Big Picture : Risk is back "On"

Global policies are pro growth yet inherently inflationary

The Week That Was

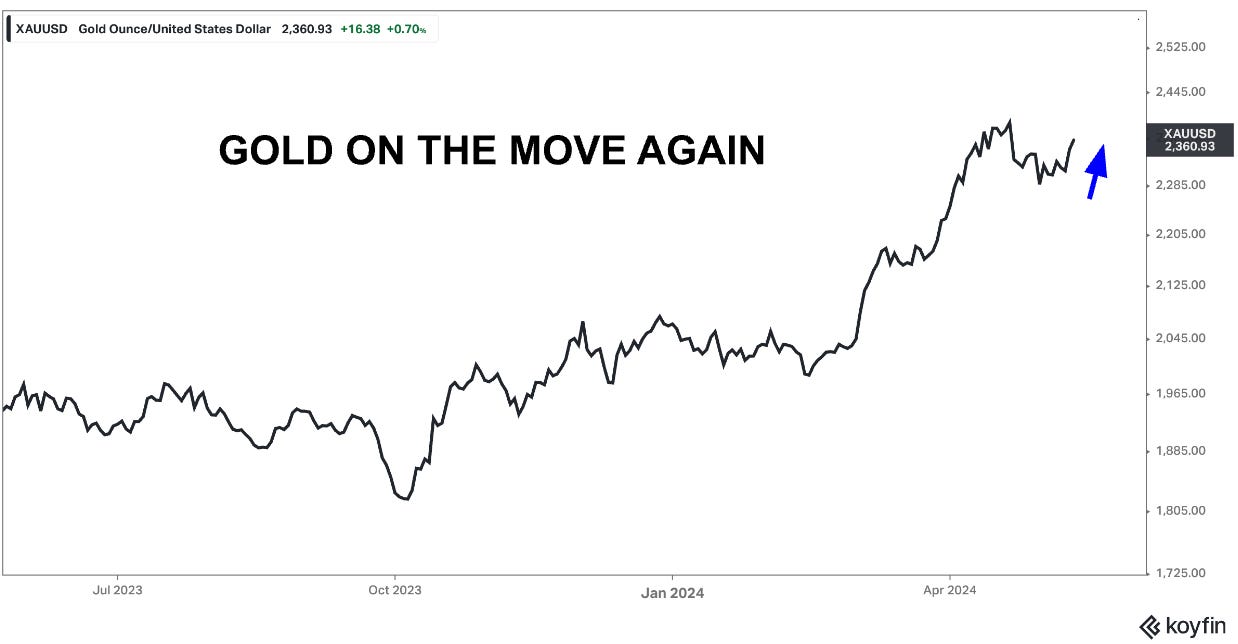

Markets have been buying gold, buying equities and selling Oil this past week as appetite for risk re-emerges in global macro.

Individuals and institutions are seeking protection from global monetary policies that are inherently inflationary while at the same time buying assets that will benefit from pro-growth central bank policy. Performance of Chinese assets and Chinese central bank action are a perfect illustration of this unique dynamic. I now bring to your attention two charts. The chart of gold and the chart of the FXI mainland Chinese ETF. Both are taking off.

Market participants are buying gold as an inflation hedge and recent data released on Chinese FX Reserves indicate further accumulation of gold by Chinese authorities. I look at this accumulation of gold by China as a calculated large scale portfolio asset switch out of US treasuries into gold during what has been a particularly inflationary environment beyond China’s own shores.

The recent performance of Chinese ETFs, in my opinion, brings together all the major macro policy themes that have been discussed in my posts this year. These themes include rising liquidity and explicitly pro growth official policies.

Central Banks

Which ever way you look at it, central banks are easing monetary policy.

We already know the SNB is cutting rates but even in countries that are trying to hike like Japan, the central bank is still actively buying government bonds and pumping liquidity into the market. China is easing reserve requirements and buying domestic ETFs. The Fed is tapering QT and could theoretically become a bond buyer in months where treasury security redemptions exceed 25 billion in nominal terms. The ECB wants to cut as does the Bank of England. The Riksbank of Sweden has already started an easing cycle and even if certain central banks are forced to delay some rate cuts the promise remains further down the line. As discussed in earlier posts numerous times, this “promise” is extremely powerful.

It signals to markets, “Don’t worry…lower rates are coming. “

Final Word

Ultimately whether current official policies prove to be prudent or not will be decided by where global underlying inflation sits in six months time. In countries where mortgage debt is high like in Sweden and Canada, inflationary impulses seem to be dissipating. Chinese inflation remains soft as well. But a re-emergence of momentum in US and European inflation data is now evident and I do worry about this upward momentum being further fuelled by rising liquidity and easing monetary conditions in global asset markets.

Markets can tolerate inflation of up to lets say 3%, but anything north of that will require central banks to shut the liquidity taps and start talking tough on inflation again.

Until that time however, the global “party” in both gold and risk assets is likely to continue.

As Always we shall keep you posted here at Purity Macro.

If you enjoyed this post, please be sure to like, comment or share the link with a friend.

You can also now follow me on notes : @puritymacro

Disclaimer

The information provided in this post is for general use only and does not constitute a solicitation for investment. It should not be construed as professional financial advice. Seek independent professional consultation before making an investment decision.

It does strike me that we are setting up for a cooler CPI on wednesday. I especially liked the news that the BLS removed coffee from the measurement, seemingly because it rose so much and was skewing things even though it is a small part of the calculation.

There is no doubt that the government, writ large, is anxious to show that inflation is lower, at least in the data, such that the Fed can finally start to cut rates as they so desperately would like to do. I have been a skeptic that the Fed would actually push to try to help ensure that Trump is not elected, and in their mind, it seems clear that they believe cutting rates will help Biden. But it is not clear to me why that is the expectation. After all, if they cut and the price pressures that people actually feel, not the ones measured by the BLS, rise further, that will only help Trump more.

I want to believe they are ignoring the election, but it is getting harder to do so. that said, if we see a cooler number than forecast, we will certainly see a risk rally!