The Big Picture : Preparing for a September Rate Cut

July 13, 2024

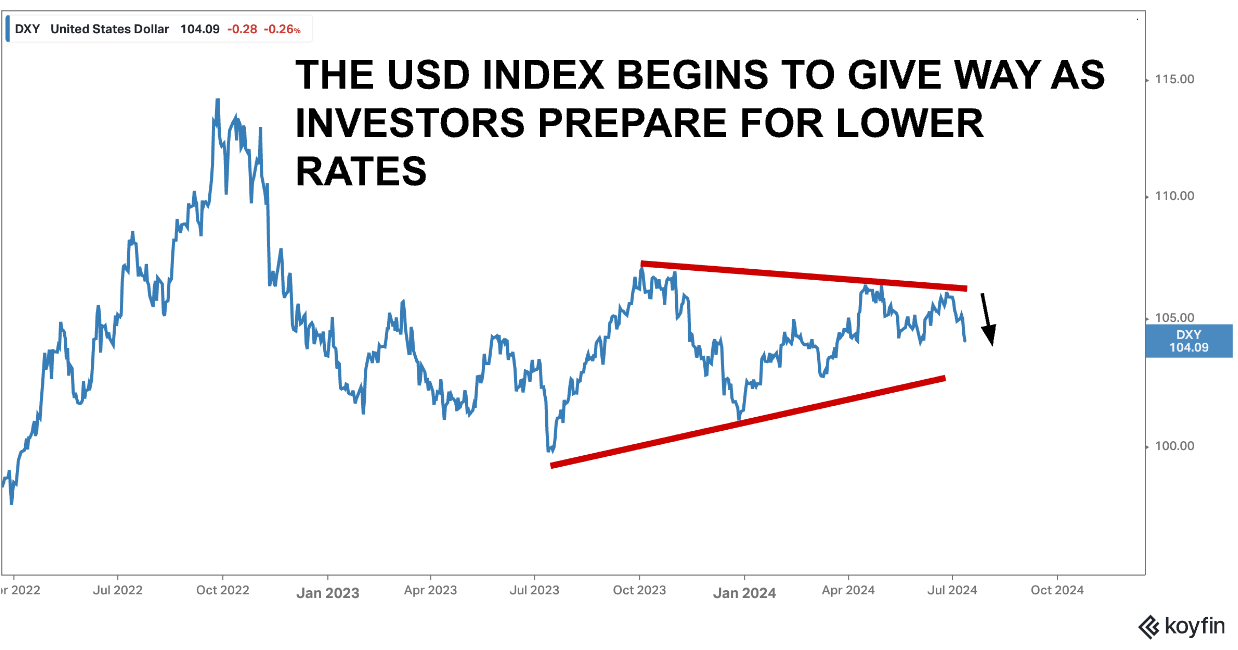

The Week That Was

Markets became convinced this week that ongoing global disinflationary processes will lead very soon to lower overnight interest rates in the US. The Dollar sold off, equities rallied and fixed income curves steepened in anticipation of a definitive signal expected to be made by Chairman Powell at its upcoming Fed meeting, scheduled for the end of July, that lower rates are now indeed warranted.

The Chairman will be emboldened by the release of this week’s US inflation data, which came out softer than expected, and at the same time be concerned by recent upticks in the unemployment rate.

You must recall that his explicit mandate is too keep inflation at or below 2% while maximizing employment. If recent trends in both the monthly inflation pace and the unemployment rate continue, the Fed Chair risks falling “behind the curve” in a crucial quarter for the US economy.

Central Banks :

European and Canadian central bankers must also make their individual decisions regarding further rate cuts as they prepare for their upcoming July meetings.

Canada will be in a much better position to make this decision after seeing June’s CPI data, which is expected to be released on Tuesday of this upcoming week.

May Cpi data indicated a short term resurgence in Canadian price pressures and the Bank will need to ascertain as to whether this was a one month blip or something more concerning. Further information on Canadian activity will also assist the Bank in gaging the underlying trend of growth. To that end, releases of June CPI, the Business Outlook Survey and Retail Sales out of Canada, all expected to be released this upcoming week, will be closely watched in order to determine whether the BOC will deliver back to back rate cuts at its July meeting.

Over in Europe, the ECB are expected to meet this upcoming week and provide a summary of their outlook on monetary policy going forward. Markets are not looking for a rate cut at this meeting, preferring to see the ECB cut again in September as it seems that is what Christine Lagarde of the ECB has implied at her various speeches delivered on monetary policy in the past few weeks.

Looking Ahead

Markets will continue to focus on sector rotations in the US, both in the Fixed Income and the Equity market, as we brace for lower rates.

Housing data out of the US, scheduled to be released this week, will be particularly watched given recent weakness….along with a Powell speech scheduled for Monday.

We also are set to receive data on US Retail sales, Industrial activity in Europe and inflation out of Japan in addition to key price and activity indicators for the Canadian economy. Let us see how the week evolves.

As always, I shall keep you posted here at Purity Macro.

If you enjoyed today’s post please be sure to like, comment or share the link with a friend

You can also now follow me on Substack’s notes : @puritymacro

Disclaimer

The information provided in this post is for general use only and does not constitute a solicitation for investment. It should not be construed as professional financial advice. Seek independent professional consultation before making an investment decision.