Macro Notes

Market bullets for June 6th, 2024.

Global Macro:

Bond Volatility is rising with the average daily net change in 10y rates markedly higher last 2 weeks

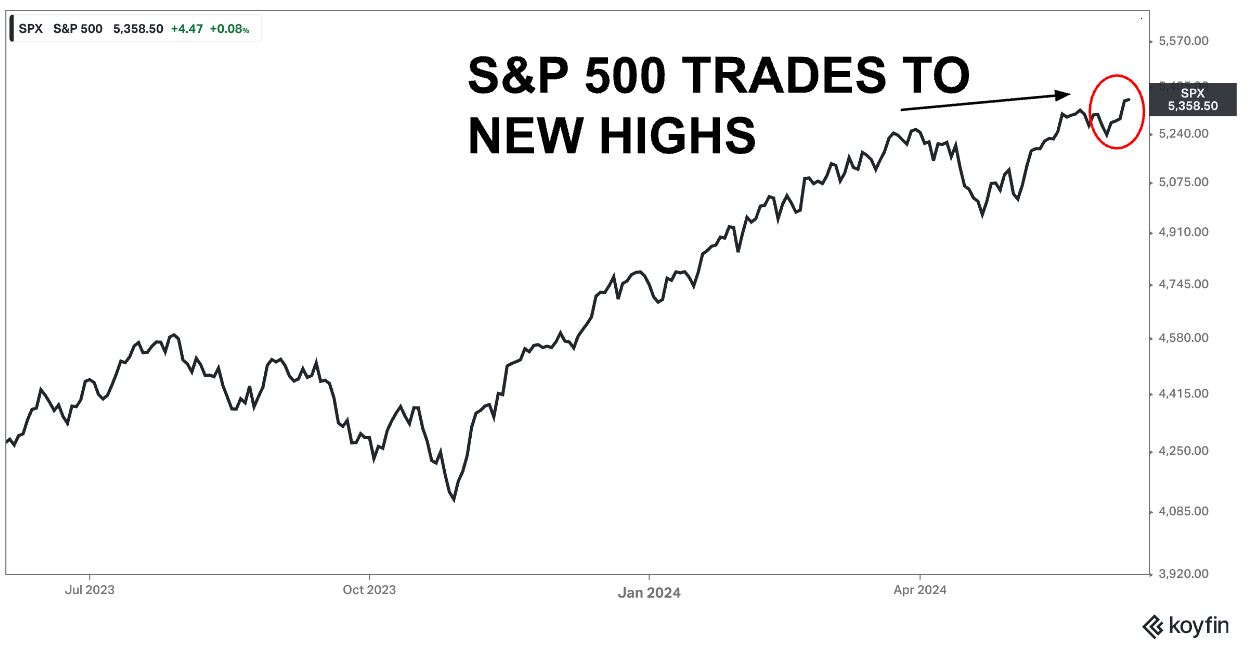

S&P 500 breaks to all time highs as G7 monetary policy easing begins.

Crude oil futures break below $70.00/barrel for contracts trading for delivery towards the end of 2025. Minor builds in inventory noted this week but prices may remain supported in the short term as technical support levels are hit on the charts.

Ecb policy

The Overnight depo rate was by 25 basis points despite slight upward revisions to inflation forecasts for 2025.

The panel is increasingly confident that a disinflationary process is now firmly underway and we expect the Ecb to reduce rates by 25 basis points at every other meeting. That would mean we expect a total of 50 basis points of further cuts this year, roughly the amount that is currently priced into the short term money markets.

Euro and Euro FX crosses are marginally higher today despite the rate cut as the Ecb currently is unwilling to provide markets with a clear easing rate path choosing instead to take each decision meeting by meeting. This is a prudent approach in our opinion as spot headline inflation rates currently remain above its stated target.

In today’s press conference, Governor Lagarde mentions particular attentiveness going forward to the evolution of wages and major government and private sector pay rounds in order to gage the second round effects of inflation. It seems the ultimate amount the Ecb can ease will be to some degree contingent on the outcome of these wage rounds.

Bank of Canada Policy

The Bank cut it’s overnight rate of 5% by 25 basis points to 4.75%. 3 month annualized measures of it’s preferred Trimmed Mean gage of Cpi have been more in line with an eventual 2% target and therefore the BOC felt comfortable enough to be able to move in order to actively support the economy.

More rate cuts are expected and given the Canadian Dollar’s historical vulnerability to interest rate differentials it would be reasonable to expect some weakness relative to the Dollar as the BOC has begun easing in advance of the Fed.

This bout of currency weakness should be temporary however as we anticipate that Fed rate cuts should also ensue imminently.

Fed Policy

Core pce has started to weaken with the shelter component in particular coming in at a significantly weaker pace relative to prior months

Growth and activity data on balance have been weaker then expected last 8 weeks and we expect the Fed to now commence an easing cycle starting from it’s July monetary policy meeting

Money market futures have started to reprice Fed rate cuts in 2025 but the immediate front end still seems underpriced given our outlook that an easing cycle is now imminent

As always, we will keep you posted here at Purity Macro

If you enjoyed today’s post, please be sure to like, comment or share the link with a friend.

You can also now follow me on notes : @puritymacro

Disclaimer

The information provided in this post is for general use only and does not constitute a solicitation for investment. It should not be construed as professional financial advice. Seek independent professional consultation before making an investment decision.

It seems you are still in the minority calling for a July cut by the Fed. I think we will need to see a substantial downtick in data for that to happen, and so far, it just hasn't been that evident