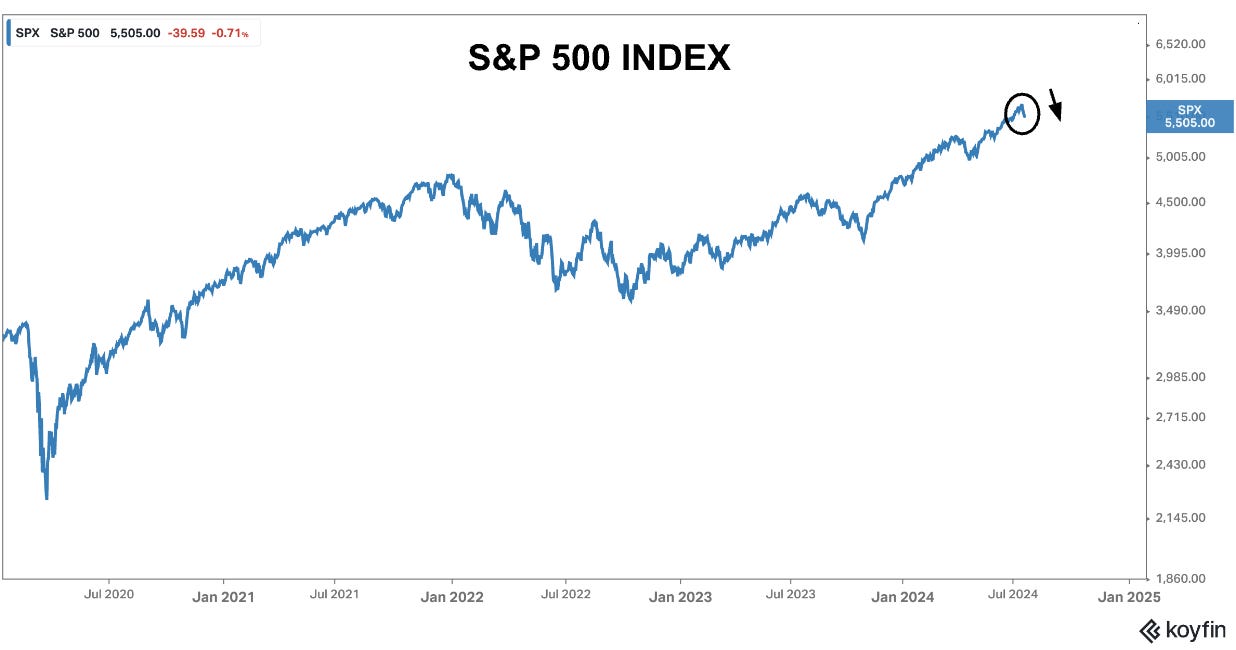

The S&P 500 has performed well this year with the main index being up some 15% in the last 7 months despite some recent losses.

A global G7 easing campaign, combined with European and Chinese economic uncertainty have led to inflows into US stocks which themselves have experienced strong corporate earnings growth and significant investments into new possibilities created by the advent of AI technology. The combination of these factors have helped to push the P.E of the S&P 500 (on a 12 month trailing basis) up towards 30, a level which would be defined as “rich” from a historical perspective.

It’s a lot easier to own US stocks when multiples are below 25, but this time around anticipation of easier Fed policy combined with post US election tax cuts are super charging a market that already had a number of bullish factors in its favour. If recent stock market gains are to be supported by corporate earnings growth in 2025 than that growth needs to be somewhere in the neighbourhood of 20 - 25% according to my calculations.

So then I ask myself is a 20-25% level of corporate earnings growth realistic based on the current macro-environment?

Now we know that historically Eps growth rates correlate well with GDP growth at a multiplier roughly around 10. This means that for every 1% of growth in Gross domestic income, you can expect 10% growth in corporate earnings. If the current S&P 500 level is to be justified from an Eps valuation perspective then that would mean the US economy needs to grow by around roughly 2.5 % next year. A 2.5% growth rate should translate into a 25% growth rate in corporate earnings growth, all else being equal.

The Fed’s own models forecast a 2% growth rate for 2025, leaving the additional 50 basis points of growth to possibly come from an economic boost post US elections. That is not unrealistic to expect based on recent spending records of both democratic and Republican administrations.

No doubt, the US economy is currently slowing….election uncertainty looms and we are still about 2 months away from the advent of easier monetary policy. Has the stock market over extended itself in the short term pricing in a bright 2025 while current conditions remain sub-optimal? Perhaps. Fast spec money in Tech stocks and sector rotations into small caps are also creating disruptions in the marketplace but barring a significant growth or inflation shock from here or a hung US election result, it would be difficult for me at this point to see the justification for a meaningful and lasting selloff in US equities from these levels, all else being equal.

But as always, I shall keep you posted here at Purity Macro.

If you enjoyed today’s post please be sure to like, comment or share the link with a friend

You can also now follow me on Substack’s notes : @puritymacro

Disclaimer

The information provided in this post is for general use only and does not constitute a solicitation for investment. It should not be construed as professional financial advice. Seek independent professional consultation before making an investment decision.

Interesting! What do you think are the possibility that the equity market trades sideways in the lead up to the US Elections? Like you mentioned, there is no real reason for the markets to sell but a stronger than expected Kamala campaign and spotty inflation prints might give markets little reason to buy due to uncertainty. I have not really formed my own thoughts regarding this but interested to hear what you think