The Big Picture : The Dollar is King

The Big Picture : The Dollar is King

In this week's Big Picture series we provide a top down macro-economic perspective on our core US Dollar view.

The Week That Was

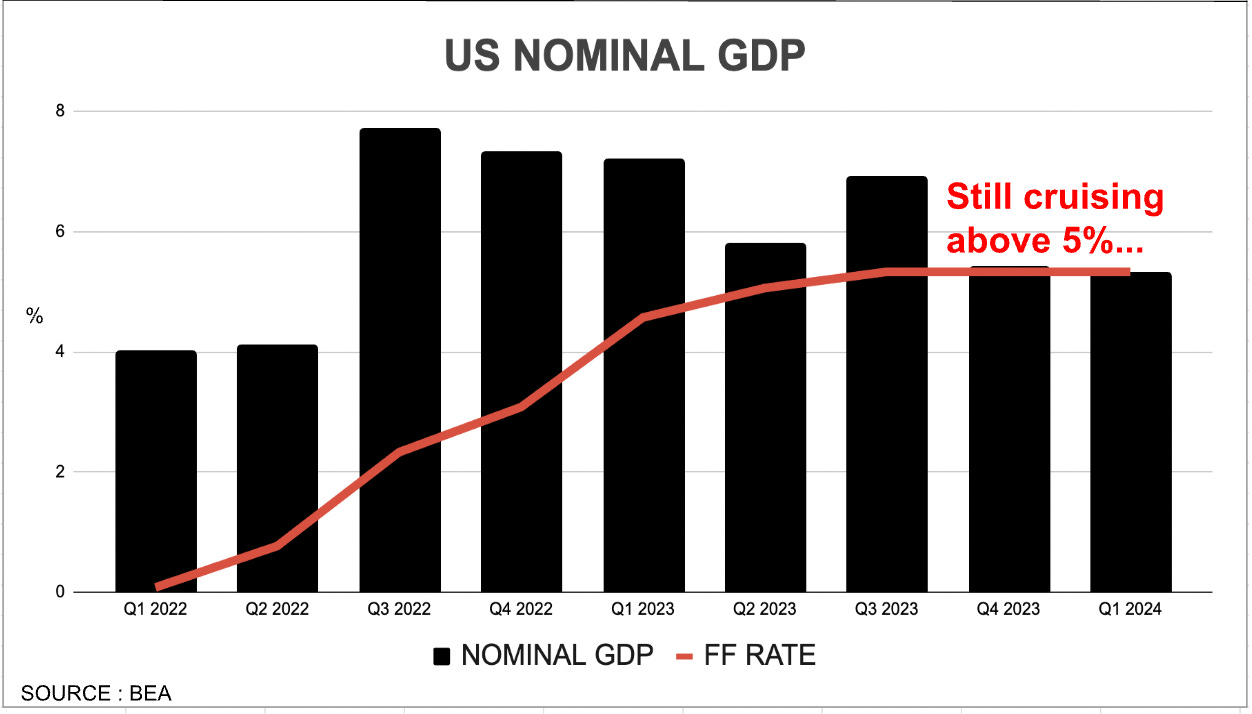

US GDP figures, released this week, showed a US economy that continues to grow above 5% annually from a nominal perspective, albeit with a slightly worse growth vs inflation mix thus far this year.

Recall that Nominal GDP = Real GDP + Inflation. On that calculation see below the results for both Q4 of last year and Q1 of this year.

Q4/23 GDP GROWTH : 3.4% (real growth) + 2% (inflation) = 5.4% (Nominal growth)

Q1/24 GDP GROWTH : 1.6% (real growth) + 3.7% (inflation) = 5.3% (Nominal growth)

As you can see the growth vs inflation mix has indeed moved unfavourably this quarter(1.6% real growth vs 3.4% last quarter and 3.7% inflation vs 2% last quarter) but this outcome at least from a growth perspective isn’t cause for concern just yet.

Weakness was mainly seen in Durable Goods consumption and Net Trade numbers both of which can be highly volatile. Strength in Services and Investment still indicate to us underlying economic strength. The growth in those sectors combined with the resumption of upward momentum in prices will send a clear signal to the Fed that overnight policy rates north of 5% are still warranted.

The Fed

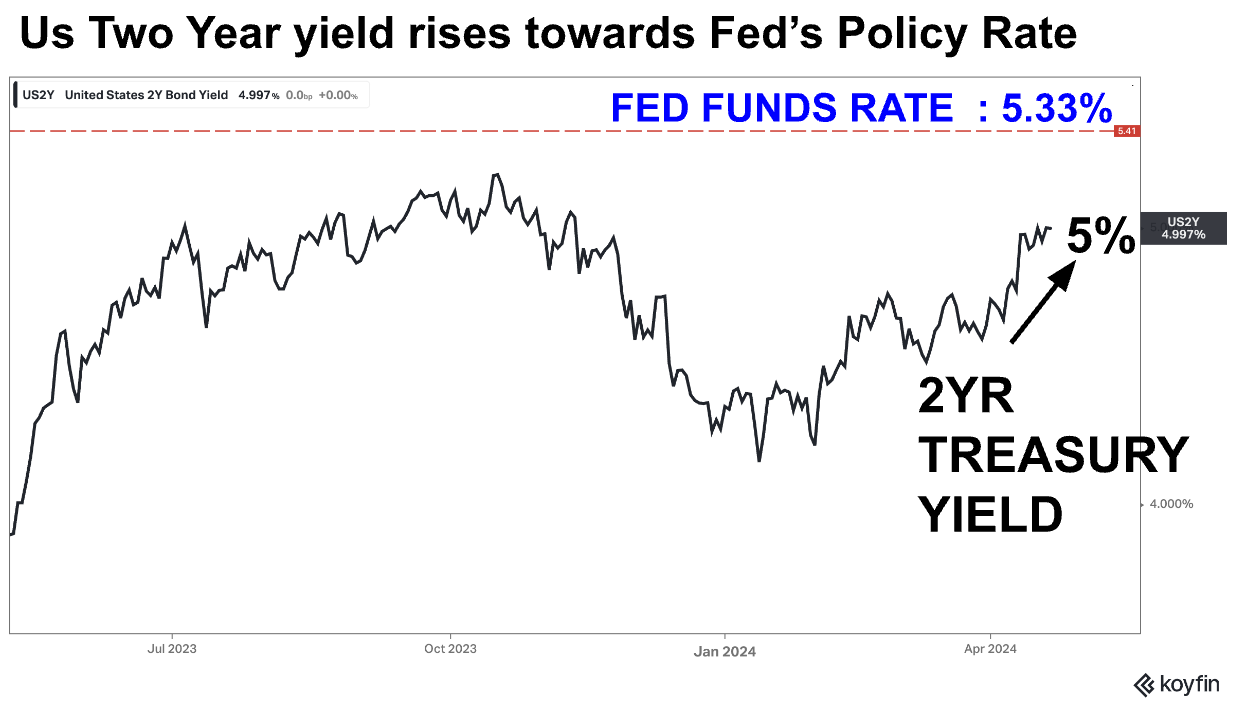

The Bond Market has now very well understood this equation and rightfully pushed two year treasury yields towards the Fed’s Overnight policy rate of 5.3%(as we can see from the chart above).

Despite the slightly worse growth vs inflation mix, the Fed will have no choice but to keep policy rates restrictive until Nominal GDP growth clearly begins to exhibit a downward path.

While Nominal GDP growth in the US remains at 5%, short term US bond yields and the Fed’s overnight policy rate will also need to remain at or near 5%.

A 5% policy rate combined with a 5% Nominal GDP growth rate in the US will ensure a sufficient yield gap between the US and its major trading partners to maintain upward pressure in the broad dollar, all else being equal.

The Week Ahead

It’s an important week on the data front :

US - Key Housing Data, Jolts and Non Farm Payrolls

Canada - Feb GDP and BOC Governor Macklem speeches

Europe - Q1 GDP and April Flash CPI Estimate

Japan - Retail sales, Industrial Production and BOJ Minutes

ECB Rate Cut watch : We’ll be particularly keen to watch the release of Q1 GDP estimates and April’s flash CPI estimate out of Europe as these figures will have a direct impact on the ECB’s next monetary policy decision scheduled for June the 6th.

As Always we shall keep you posted here at Purity Macro.

If you enjoyed this post, please be sure to like, comment or share the link with a friend.

Disclaimer

The information provided in this post is for general use only and does not constitute a solicitation for investment. It should not be construed as professional financial advice. Seek independent professional consultation before making an investment decision.

It would be a big change indeed but Powell is intrinsically dovish. And now GDP growth slowed down as well. From an economic perspective, they absolutely should hike again and kill inflation. But these guys walk up to congress hill every week and get their ears filled with complaints from congress men/women about employment, growth etc. Election year too....let's see

I wonder, after Williams mentioned the idea of a rate hike later this year, do you think that will get credence in the discussion this week? That would be a massive change in view, I believe