The Big Picture : A Tale of 3 Central Banks

The Big Picture : A Tale of 3 Central Banks

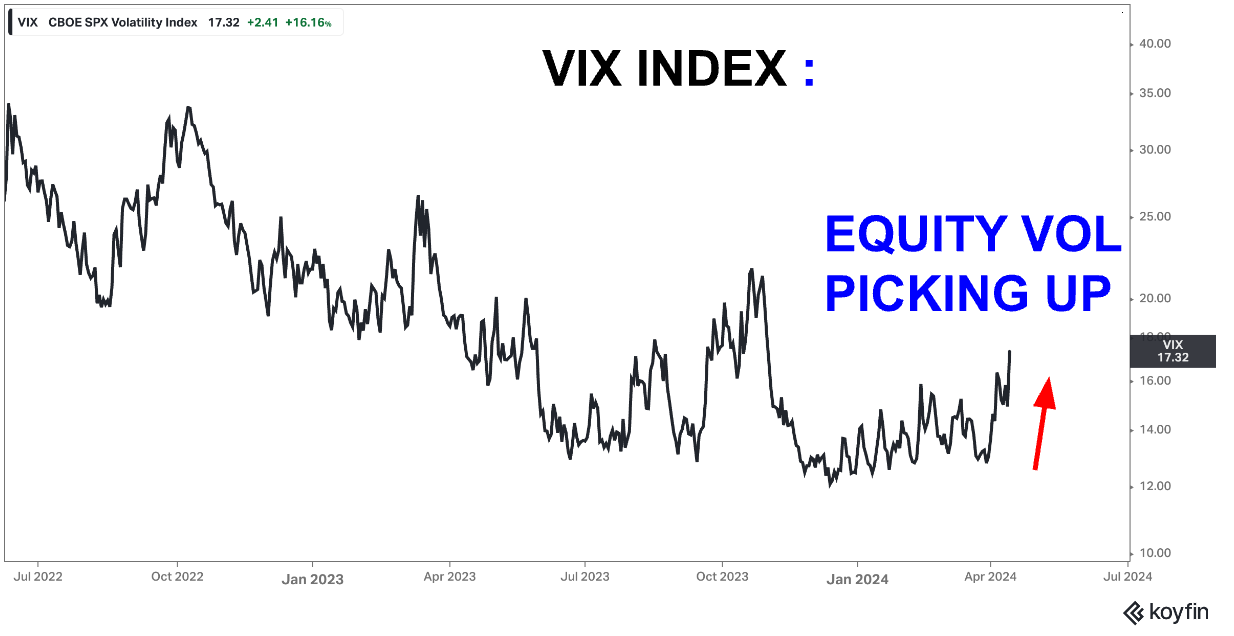

In today's piece we discuss differing central bank narratives and drivers of rising volatility in global markets.

The Week That Was:

Unfavourable trends in US inflation, rising geo-political tensions and weak Chinese economic data pushed equity prices lower and volatility higher this week.

The market is in risk reduction mode and a safe haven bid in the Dollar is now apparent.

Inflation breakevens are rising and financial conditions are tightening.

We are watching the 2.5% level in 10yr US Inflation Breakevens as a potential trigger for a more explicit shift in the Fed’s tone towards a more hawkish stance.

Long-term inflation expectations must remain anchored at all costs.

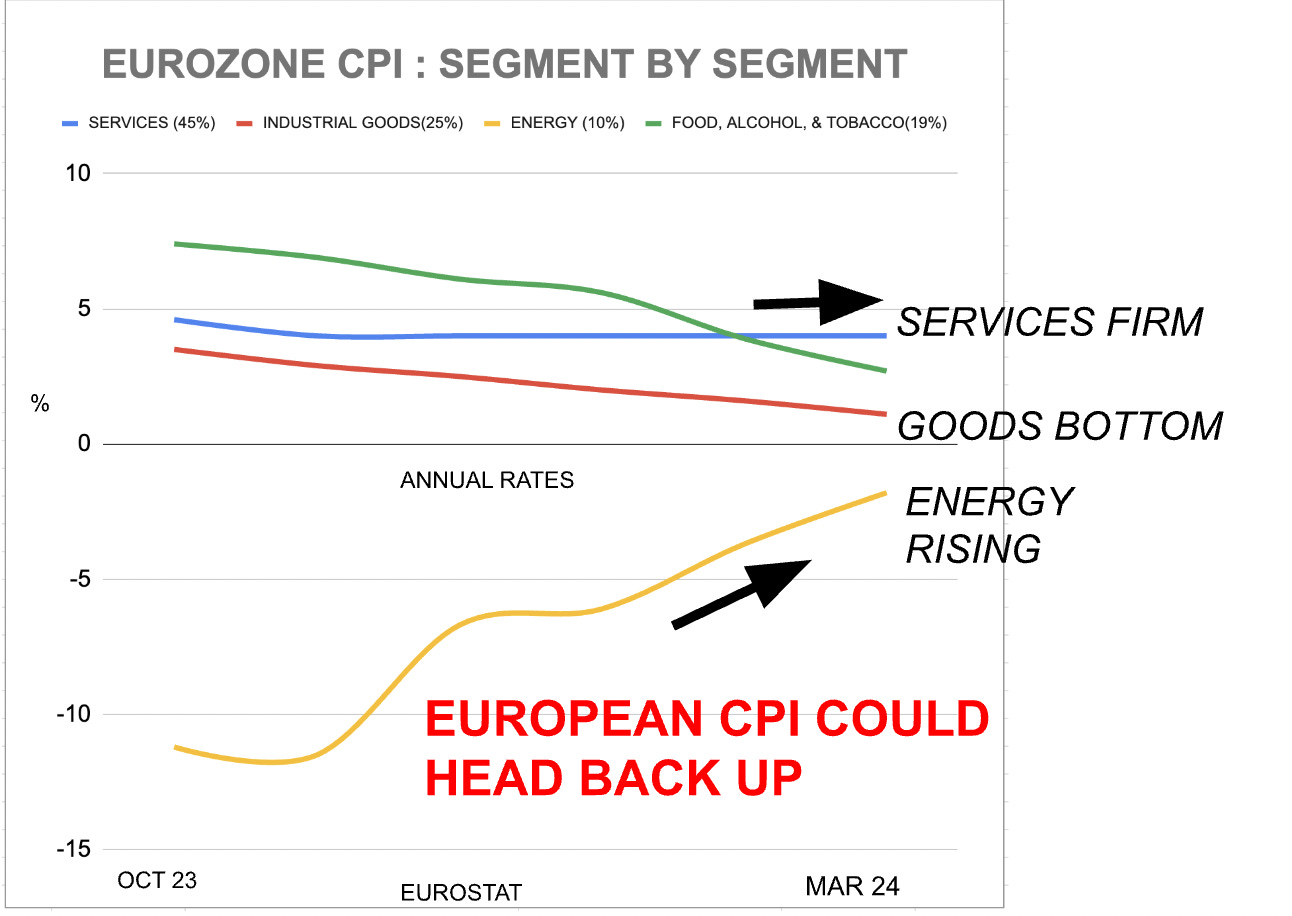

Rising inflation concerns in the US were juxtaposed with dovish rhetoric from both the ECB and the BOC this past week, pushing European/Canadian yields lower and widening the interest rate gap in favour of the US Dollar.

Central Banks:

We now have clearly differing narratives amongst central banks in the US, Europe and Canada.

The US wants to normalize policy but is being held back by a strong economy and short-term inflationary trends which threaten to send inflation back above 3%.

The ECB is looking to cut rates even as short-term inflation trends are rising. They remain convinced that the recent “spike” in monthly measures is short term in nature and must be looked through.

The Bank of Canada would also like to ease policy.

Recent labor market reports have been weak, business sentiment has softened and underlying core inflation trends have cooled.

Whether Europe and Canadian monetary policy can meaningfully diverge away from the US is still yet to be seen however. A rising US dollar threatens to send more inflation to the shores of its trading partners limiting their ability to begin easing policy until the Fed feels ready to so.

The Week Ahead

The global economic calendar is packed this upcoming week.

In the US we have retail sales, IP/Capacity Utilization, Oil Inventories, Fed’s Beige Book, US Jobless and Philly Fed.

Canada gets key CPI data on Tuesday while Europe receives final readings on March inflation. The UK is set to release employment, CPI and retail sales. Japan releases March Inflation data and markets will keenly wait for Q1 GDP out of China along with other activity related measures set to be released on Monday.

As Always we shall keep you posted here at Purity Macro.

If you enjoyed this post, please be sure to like, comment or share the link with a friend.

You can also now follow me on X : @puritymacro

Disclaimer

The information provided in this post is for general use only and does not constitute a solicitation for investment. It should not be construed as professional financial advice. Seek independent professional consultation before making an investment decision.