Macro Notes

Macro Notes

In today's Macro Notes we discuss the recent "melt up" in global bond yields, decipher today's US Q1 GDP release and discuss the prospect of steeper curves in Europe.

Melt up in Global Bond Yields

10 year rates are spiking globally on the back of 2 major macro-economic factors:

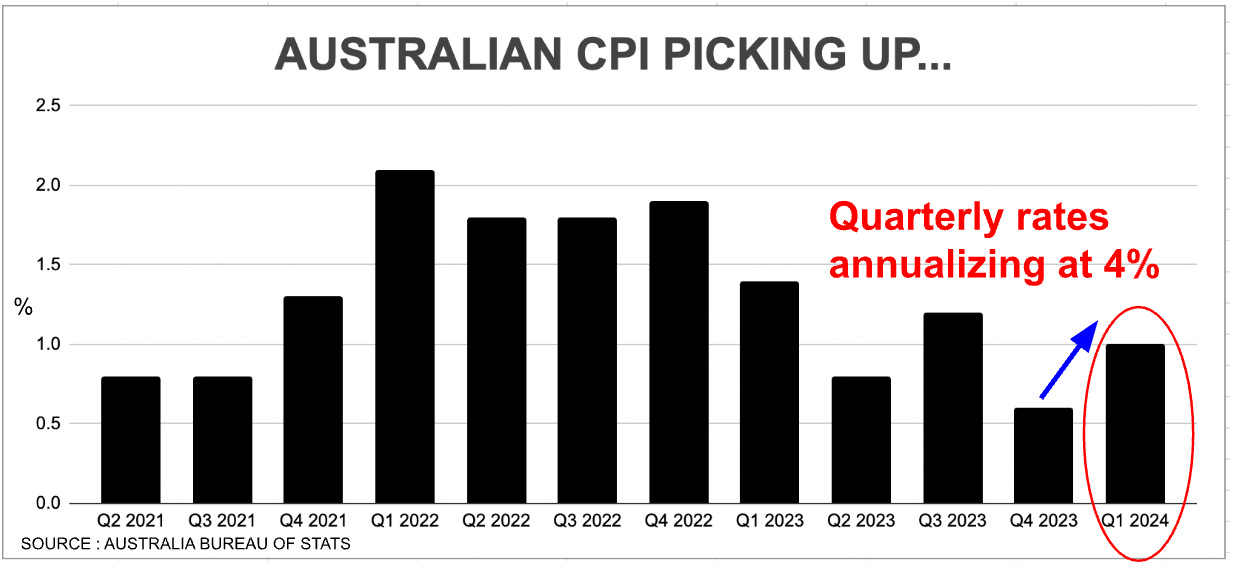

It is becoming increasingly clear that annual inflation rates are in no mood to ease any further. Global service and housing related inflation remains firm while underlying energy pressures remain. Core PCE quarterly rates embedded within today’s US GDP report and CPI data released by Australia earlier this week are further proof that pipeline price pressures remain.

Easier monetary policy from Non US Central Banks will steepen curves and force long-term yields higher. China will be stimulating, Japan is still buying JGBS, the Swiss National Bank is cutting rates and both the Bank of Canada and ECB will begin modest easing cycles this summer. As foreign central banks lower interest rates faster than the US, their currencies will depreciate thereby driving global inflation rates even higher.

Bond Markets, fretting over this upcoming reality, are adjusting to the new inflationary paradigm.

US GDP

The advanced estimate of Q1 US GDP was released today with some interesting and perhaps even puzzling takeaways for markets.

The quarterly growth number came in much weaker than expected : +1.6% for Q1.

This result was below both our and the markets expectations. Recent tracking models at the Atlanta Fed had been predicting a number closer to 3%. On the face of it, this 1.6% print could be taken as an early sign that growth is beginning to meaningfully slow down in the US, as had been feared by the Fed last year.

We would however caution against drawing that conclusion just yet.

Diving into the details, the slowdown was mainly driven by non cyclical and volatile components of GDP such as durable goods, and net trade.

It’s too early to judge whether weakness in these segments are temporary or signs of something more meaningful. Especially while labor markets and production data indicate a still robust economy.

The pace of government consumption expenditures also unexpectedly slowed to 1.2% this quarter, down from a 4.5% pace throughout 2023. We fully expect this to bounce back next quarter. Government spending numbers should remain fairly predictable from 1 quarter to the next. Key cyclical elements of the report however such as consumer service expenditure and domestic investment were impressive, both growing faster than the preceding quarter at a rate of 4% and 3.2% respectively.

Core PCE prices for Q1 also printed much higher than expected at 3.7%. This now poses upside risks to tomorrow’s monthly core PCE data for March.

Bottom Line : Weakness in growth numbers were driven by segments that are volatile (eg. Durable Goods) or by parts of the economy that are likely to bounce back next quarter (eg. Government expenditure).

In the meantime, the higher Core PCE prices for the quarter will keep bond markets on the back foot.

Curve Steepening in Europe

Dovish comments from ECB members combined with stronger PMI and IFO data out of Germany steepened the 2s10s yield curve by 12 basis points this week.

This is a trend we think is likely to continue. As the ECB forces short end rates lower, the long end will be forced up in yield by concerns on inflation and a weaker currency.

We discussed in our Macro Notes deep dive last week, as to why we think the Euro is set to materially weaken. Click on the link below if you missed it.

https://puritymacro.substack.com/p/macro-notes-214

A further 5 to 7% correction lower from here in the Euro will ensure the steepening trade in Europe remains intact all else being equal.

All eyes now on Core US PCE numbers tomorrow.

As Always we shall keep you posted here at Purity Macro.

If you enjoyed this post, please be sure to like, comment or share the link with a friend.

You can also now follow me on X : @puritymacro

Disclaimer

The information provided in this post is for general use only and does not constitute a solicitation for investment. It should not be construed as professional financial advice. Seek independent professional consultation before making an investment decision.

But you didn't mention the BOJ tonight!