Big Picture : Monthly Edition

Big Picture : Monthly Edition

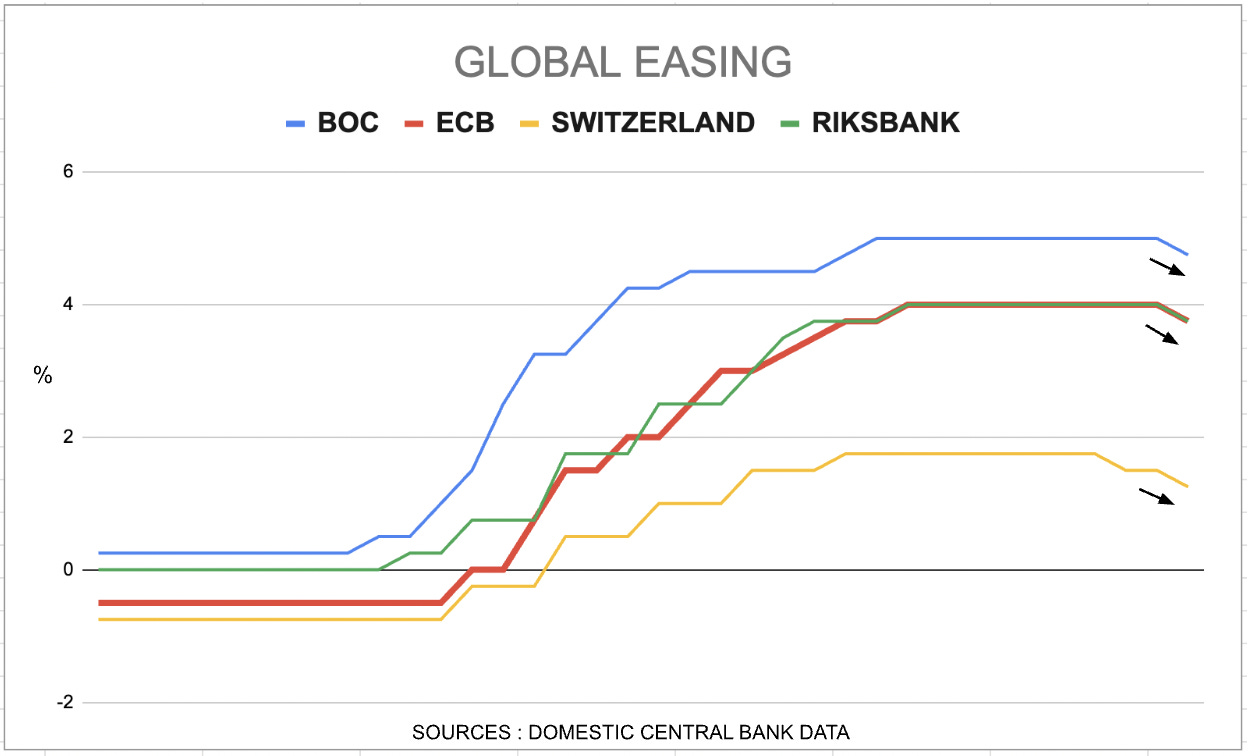

Global easing is underway

Opening Statement:

As we complete the first half of 2024, global easing is now well underway. Most G10 central banks have either reduced or are expected to reduce their overnight policy rates from historically restrictive levels. The process might be shallower and lengthier then previous easing cycles but the overall direction of global monetary policy is what ultimately drives the global macro environment.

Global Inflation:

Certain countries like Australia and Norway are still grappling with stubborn inflation, but overall the global picture as measured by the world’s two largest economies namely US and China indicate a softening underlying environment for price pressures as whole.

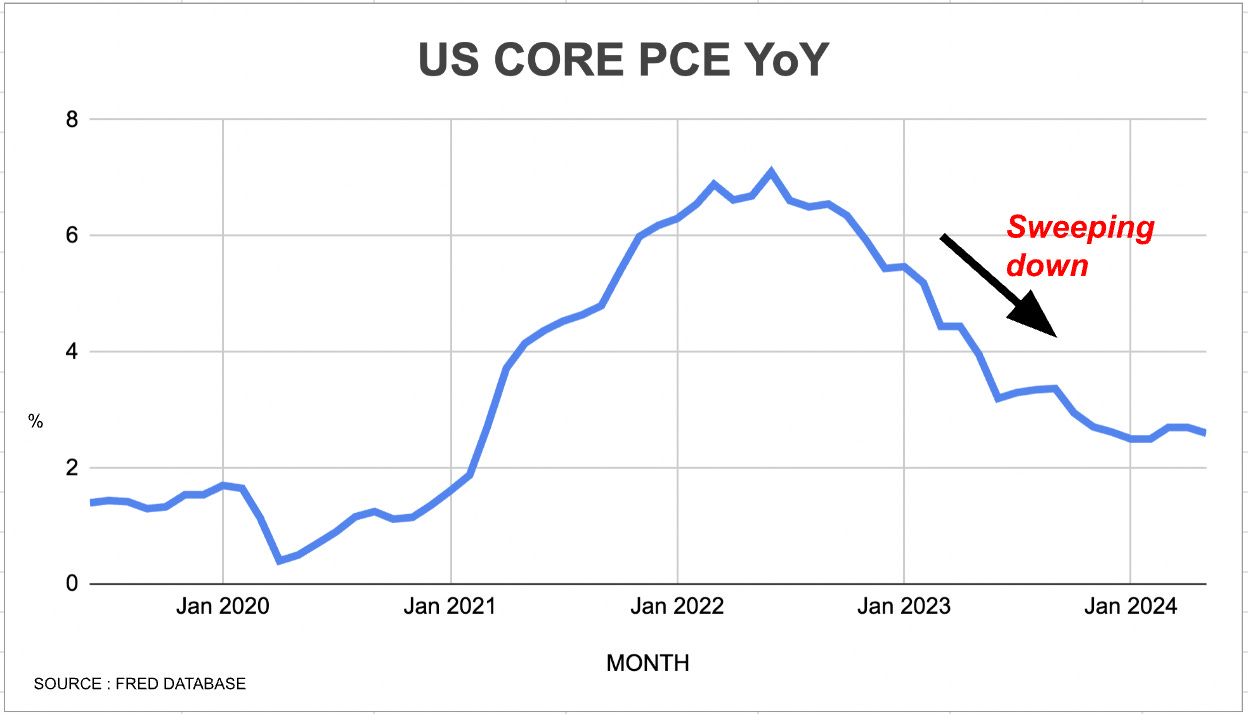

The inflation spike witnessed by the US in Q1 of this year is now, once again, giving way to a “cost of goods” driven disinflationary process which is bearing down on headline inflation.

Chinese prices are stabilizing slightly above zero, with monthly domestic price momentum unable to generate any meaningful inflationary impulse. While this is bad news for China, global trade and demand links will feel the impact of softer Chinese price pressures and this outcome will ultimately have the effect of removing additional upside risks to both US and European imported inflation.

Global energy markets however will remain a key upside risk to inflation as we head into the summer. Geopolitical risks continue to simmer and recent upticks in various energy markets once again threaten headline inflation rates. But central banks will growingly see these energy shocks as exogenous and remain hyper focused on true core measures of prices which as mentioned before show clear signs of softening, especially when we look at the US and China.

China:

On top of softer prices, domestic asset markets in China have once again begun to deflate after healthy gains were seen in the first half of this year. Chinese rates across the yield curve push lower sending a deflationary signal to markets while authorities try to instigate a managed depreciation of their currency. Plenum talks are weeks away as authorities look to announce new measures in order to support the economy.

Deflation is a disease that needs constant administration of stimulus medicine or an an outright guarantee that the central bank stands ready to buy assets , the way the Fed announced QE in 09 or the Ecb announced Peripheral Bond buying back in 2012.

Both myself and the market now keenly await what new steps the Chinese are willing to take in order to support their economy before formulating a firm view on the evolution of inflation and growth in China for the second half of 2024.

Asset Prices:

Global asset prices should remain supported overall as G10 monetary policy easing continues and core price measures soften. Chinese asset performance has decoupled from global indexes with the only real threat to global equities now being a sudden short term spike in energy prices or a credit event in Europe due to rash French politics. In this regard, it will be important to keep a close eye on French government bond spreads to Germany and the evolving war in the middle east. A French exit from Europe for now has been ruled out but I do worry about the escalating war and casualties in the middle east.

Final Word

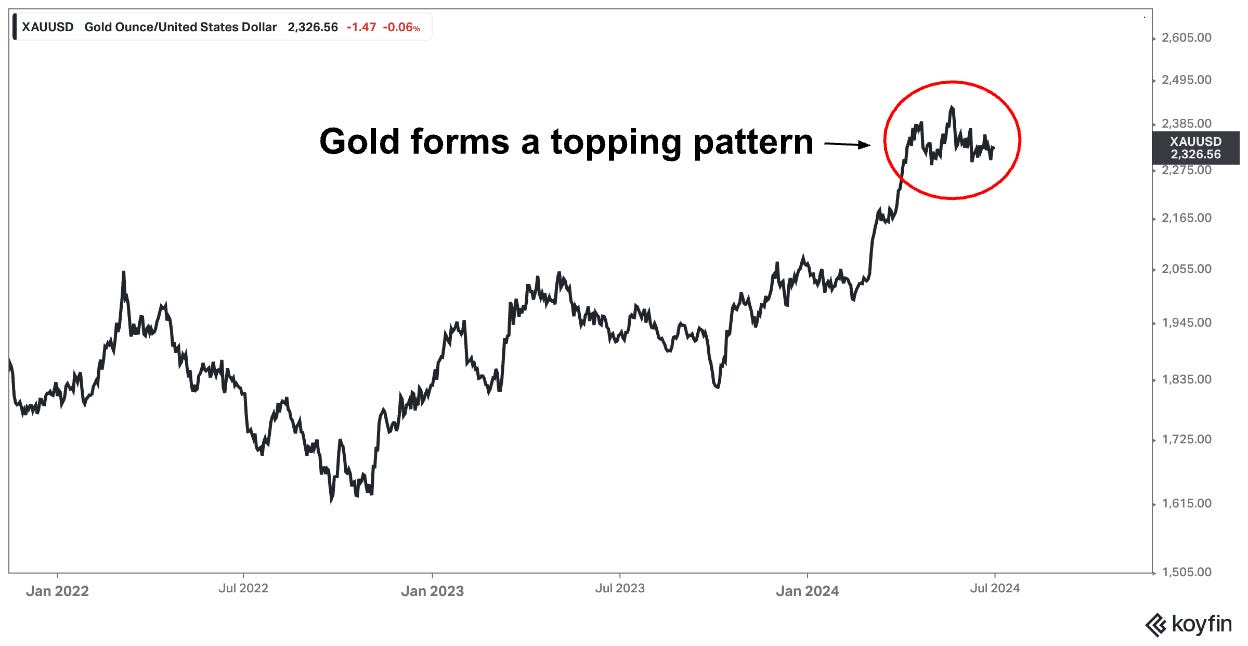

The inflation fears of the first half as reflected by the near 20% rally in the price of Gold seems to have calmed as both the Fed re-affirms its 2% target and the inflation rate itself shows signs that a 2% outcome might indeed be achievable.

If inflation will glide down to 2% at some point while the Fed begins a gentle easing to support growth, the dollar and overall long term inflation expectations should remain anchored and on the margin bias Gold lower. China perhaps should also re-evaluate its purchases of the yellow metal at the moment as that money is probably better spent on purchasing its own local assets in my very humble opinion.

A summary of my key views on major macro asset classes is included below for your review and otherwise I wish you a wonderful weekend - M.Ali

Sample Macro Portfolio