Big Picture : Fed re-affirms it's 2% target

Big Picture : Fed re-affirms it's 2% target

In this week's report we discuss German Fixed Income, US inflation and our evolving view on the price of Gold.

The Week That was

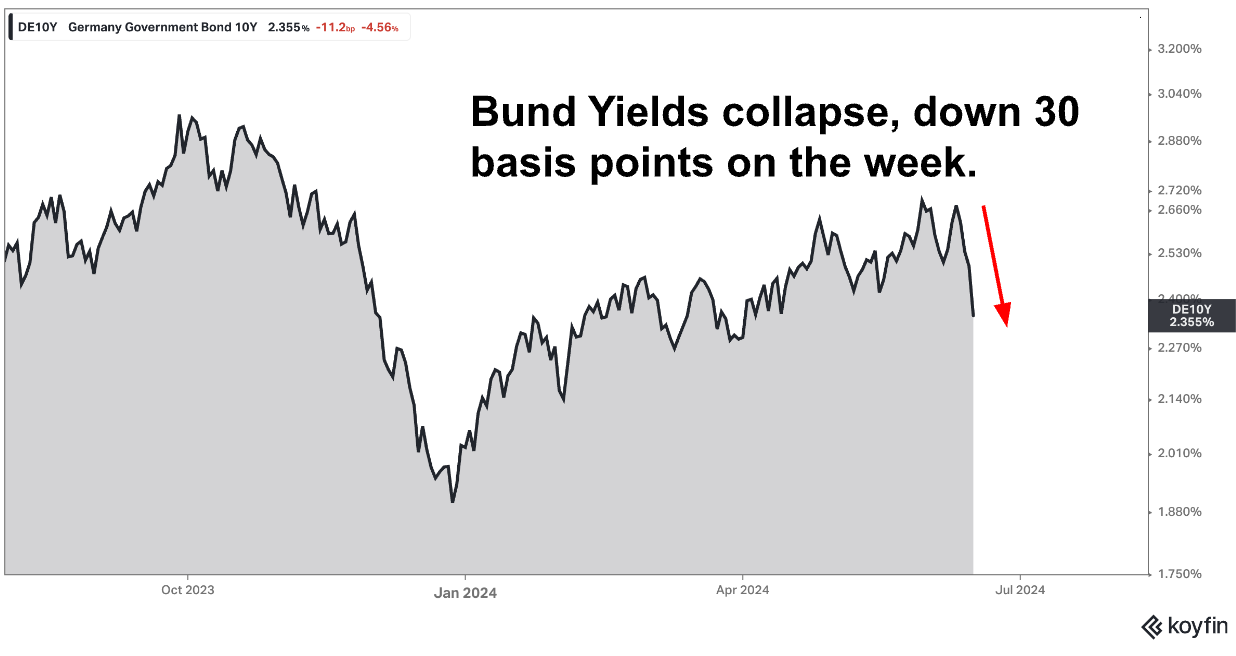

Government bond yields traded sharply lower this week driven by an uptick in European political risk, disappointment at BOJ Policy, and an unexpectedly benign US CPI report for the month of May.

US equities outperformed relative to their European peers and the Dollar traded stronger both against the EUR and the Yen with the former FX pair briefly breaching the 1.07 level before regaining support, while Usd/Jpy is now some 2% away from the all important 160 level.

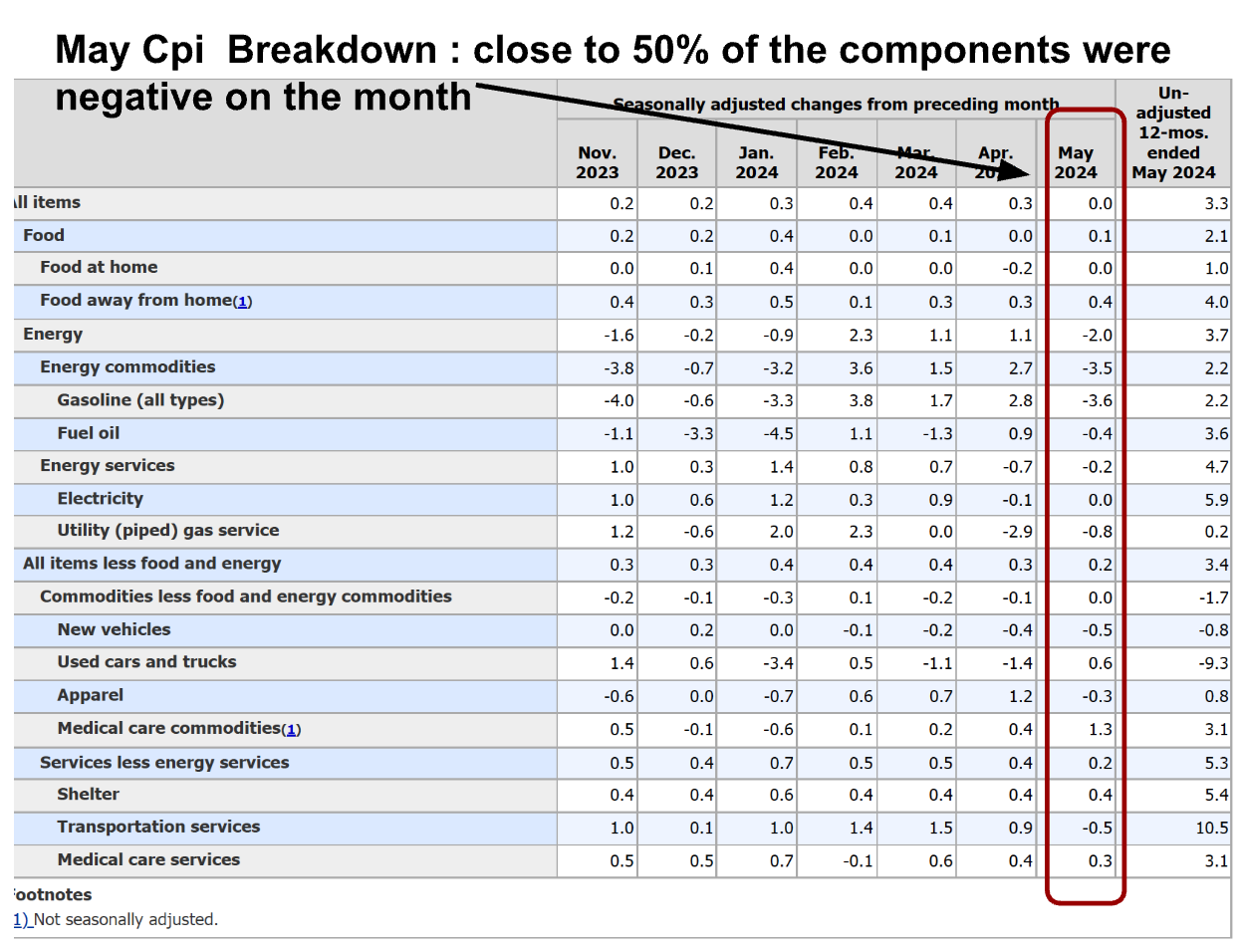

The S&P 500, remarkably, traded close to all time highs as tech stocks were driven higher by sharp rallies in both Apple and Nvidia. Money markets ignored the Fed’s hawkish dot plot revisions and instead paid more attention to May’s CPI report which displayed continuing signs of softening underlying inflation. The US fixed income curve, both in the short and long end, flattened in response to the CPI print and the Fed’s projections as the market again begins to be convinced that short term inflation orthodoxy by the Fed will lead to lower rates further out.

Central Banks

Break even inflation rates have started to collapse as the Fed forcefully re-asserts its commitment towards the 2% inflation target. In removing a full 25 basis point cut from it’s SEP projections for 2024 and revising up its core PCE forecasts a clear signal is being sent to markets that the Fed remains more unwilling to officially cut its overnight rate, like other g10 central banks, while current 12 month inflation rates remain above 2%.

It’s a surprising move.

Despite a strong jobs number in May, the U.E rate still continues to tick up and growth has clearly slowed from its torrid pace last year. I find it remarkable that the Fed has chosen to cave in at this stage at a time when there are clear signs that inflation is starting to slow and your G10 peers have crossed the rubicon and begun to ease policy.

Gold Indecision

Final Word

The Fed’s sudden re-assertion of its inflation mandate can potentially put Gold bulls in trouble. Our bullish view on Gold had been predicated on a view that Fed easing would begin prior to the 2% target being achieved. This view now must be questions in light of the the Fed’s most recent economic projections. Technically speaking, I worry that Gold is hammering out a head and shoulder’s patterns on the charts which would be confirmed if the 2,285 level is breached on the charts. Given the evolving fundamental and technical outlook, we are moving up the stop on our Long Gold position (held in our sample macro portfolio) to the 2,500/oz level until further new news arrives.

As Always, we will keep you posted here at Purity Macro.

If you enjoyed today’s post please be sure to like, comment or share the link with a friendYou can also now follow me on notes at puritymacro.

Disclaimer

The information provided in this post is for general use only and does not constitute a solicitation for investment. It should not be construed as professional financial advice. Seek independent professional consultation before making an investment decision.

Things are certainly confusing but I suspect that despite the moderately hawkish Fed, they are still desperate to cut rates and will do so at the earliest opportunity. in fact, if PCE at the end of the month is soft, I think July might be on the table. if that is the case, I love gold and all commodities and hate the dollar.